Companies with greater digital capabilities are able to convert sales at a rate 2.5 times greater than the norm, writes Graham Christie, the CCO/partner of Auckland & Sydney-based APAC-wide mobile marketing outfit Big Mobile Group in the company’s latest Mobile Hub report. Read on …

This is a term I’ve been peddling recently. It’s not mine, but I think it neatly nails a real issue that is holding back mobile. McKinsey and Company (they also admit they didn’t coin the term either), talk about it in reference to a report they have published.

In Brand success in an era of Digital Darwinism, McKinsey compiled data from 1000 brands, 20,000 consumer journeys across 100,000 touchpoints. Robust sample depth undoubtedly.

They found that competition amongst brands had heightened considerably due to digital proliferation, with the inevitable net effect that consumers were savvier, their expectations had grown, some weaker brand messages and communications had lost their impact resulting in brand impact and conversions being weakened.

Principally then, some brands have evolved their digital marketing to keep up with the consumer, some are yet to. A headline for me is companies with greater digital capabilities were able to convert sales at a rate 2.5 times greater than companies at the lower level did. Take a look at the report.

This Darwinism makes perfect sense to us; we’re living and breathing it day in day out. We see the verve and sheer velocity of digital.

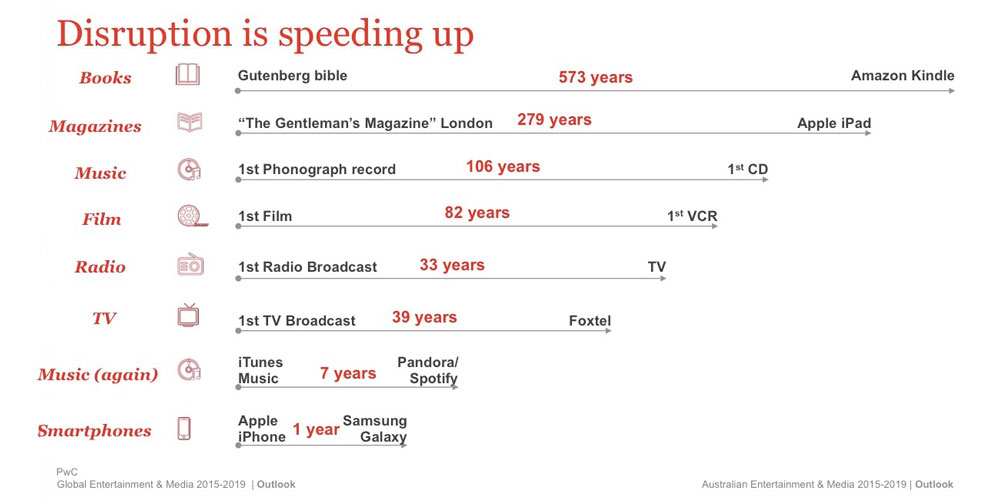

In this year’s Global Outlook, PwC included a chart that demonstrates how evolutions and in some cases revolutions in media are increasingly more and more just around the corner.

Evolutionary step

Nowhere more is this felt than in mobile, and this is surely where the biggest evolutionary opportunity is being presented today. So with a recent IAB report showing APAC remains the highest growth region for mobile in the first half of CY15, what doesn’t make sense to me is why this evolutionary step towards mobile is hesitant.

What are we concerned about? Is it that perhaps mobile will not end up being that imperative after all – surely not? Is it then that with a lack of industry measurement, it’s better to wait?

I would understand this if the cost of entry into mobile was substantial. But, in fact, it’s the very opposite. Compare for instance an advertiser budgeting for a TV campaign. So, for the sake of argument, let’s look at $200k for producing the 30sec spot, perhaps putting a $1m against it on media, then of course there’s another $200k on promo, social, search etc.

So let’s say that $1.5m on what will be a perfectly normal TVC. $1.5m! The average mobile campaign in more advanced APAC markets is between $75k-$100k, so 5% of that TV example.

With that low cost of entry, smarter marketers and agencies know that you find out a lot by testing and learning, you find the measurement that works for you. In developing APAC mobile markets where data suggests for instance China is growing by 315%, Indonesia 142%, and Malaysia 126%, there is an even greater need to evolve, such is the centricity of mobile, albeit against a backdrop of a more resilient traditional media sector. And evolve they are, and more quickly than you would think.

So Digital Darwinism is happening all around us, which side of the evolutionary line is your company and your own career on?

Mobile web vs App

This age-old question is resurrected due to a recent Opera Global report on mobile. In the US 80% of traffic is app, heavily influenced by Facebook, Game of War, Tumblr etc.

But there is only one other region of the world where this dominance is similar, and oddly it’s in some of the islands in the Pacific such as Micronesia, Melanesia, and Polynesia. Elsewhere the splits are the opposite, with web impressions outstripping app, this is especially the case in APAC.

So we should be careful not to allow the sheer heft of US-based information to automatically influence APAC thinking before looking more closely. Of course it’s not an either/or situation, nor is it just about reach, it needs to be as much about audience fit and the communication itself.

Programmatic becoming more premium

The Boston Consulting Group agrees with everybody, reporting that the $US600 billion global media sector is evolving, that word again, programmatically. In their Programmatic Path to Profit Report, they forecast that more media will be traded ‘programmatically’ by 2019 than by a direct sales channel.

It states similarities between the end of people based stock exchange trading a decade ago and where we are with digital media today to advise on not falling in to the same traps.

Fundamentally, programmatic (i.e. more automated and data enriched trading), needs to be seen as just how we increasingly execute digital communications. A means to an end, and not an end in itself.

So over the next period, there’s isn’t a single switch that will be flicked, but numerous panels of switches as the publisher concerns over depressed yields, and advertisers anxieties over quality abate.

At Big Mobile our position is to present premium audiences, leveraging tech and data, and apply a workflow and transaction model that meets the needs of the client. This means that we, and others, concurrently need to continue taking extra care and attention to develop effective mobile engagement solutions at scale in spite of a fragmented ecosystem, whilst also accelerating the development of more efficient workflows programmatically.

Agility and adaptability is the key essentially on this road to eventual vertical alignment. Being so right now is vital as we live in a mobile world under a genuine threat of an overly homogenous silicon-valley propelled ad market.

If we are not careful, and don’t learn from the stock market missteps, we’ll accelerate a commoditising effect and the true value to brand and media owner will be diluted.

Big Mobile NZ is at …

Loft 503

Level 5, Archilles House

8 Commerce Street

Auckland 1010

sales@bigmobile.com

- Rachel Blair is the Sydney-based APAC marketing director: rachel.blair@bigmobile.com

- www.bigmobile.com

- www.mckinsey.com/digital_darwinism

Share this Post