LONDON, Today: WARC’s latest Advertising Trends report, released overnight, paints a bleak picture of the impact of Covid-19 on global advertising investment.

Key takeaways are:

- Advertising investment is set to fall 8.1% (US$49.6bn) worldwide this year.

- This year’s downturn will be softer than in 2009, when the ad market fell by 12.7% ($US60.5bn).

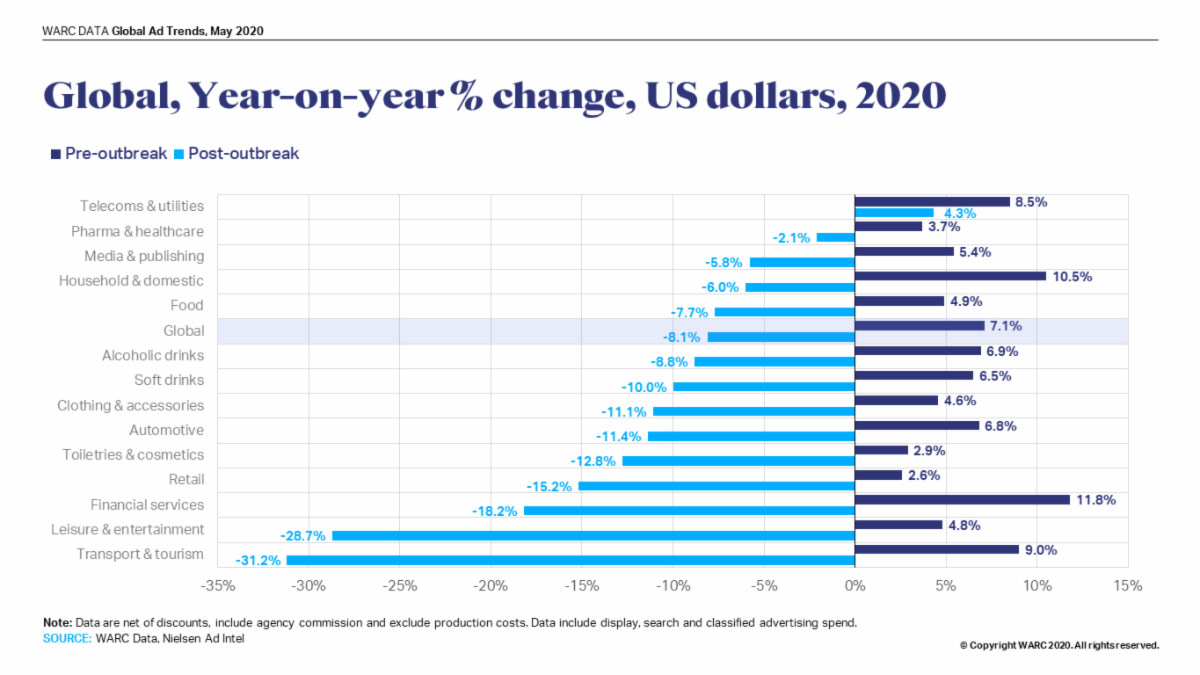

- Almost all product sectors will record a decline in ad investment this year.

- Traditional media will fare far worse than online.

- Internet advertising is set to record mild growth this year (+0.6%) at a global level.

- A recovery is forecast for 2021, at +4.9%.

The new projections, based on data from 96 markets, represent an absolute downgrade of US$96.4bn compared to WARC’s previous global forecast of 7.1% growth made in February 2020.

Traditional media will fare far worse than online, with ad investment set to fall US$51.4bn (-16.3%) this year. Declines will be recorded across cinema (-31.6%), OOH (-21.7%), magazines (-21.5%), newspapers (-19.5%), radio (-16.2%) and TV (-13.8%).

Online advertising is not shielded from the downturn; internet growth will almost grind to a halt (+0.6%) in 2020 following a US$36.5bn cut compared to WARC’s February forecast to $298.9bn. Social media (+9.8%), online video (+5.0%) and online search (+0.9%) are expected to record growth but at far lower rates than were previously projected, while online classified – particularly recruitment advertising – is set to fall by 10.3%.

Facebook’s full-year prospects have been downgraded by US$5.3bn to 11.5% growth this year, to a total of US$77.6bn, while Alphabet’s revenue is expected to grow 1.6% to US$137.1bn – $12.9bn lower than the pre-outbreak forecast of 10.4% growth.

Despite heavy downgrades across the board, the global decline in 2020 will be softer than that recorded in 2009, when the ad market contracted by 12.7%, or US$60.5bn. Record-high spending during the US presidential campaigns will stymie US ad market decline to -3.5% in 2020, while stronger-than-expected first quarter results show key media owners were in relatively good health heading into dire second and third quarters.

Almost all product categories are expected to record falling ad investment in 2020

Adspend is set to fall across almost all of the 19 product categories monitored by WARC. The travel & tourism sector is expected to record the steepest decline, with a forecast of -31.2% for 2020 representing a US$7.2bn reduction in spend compared to 2019, to a total of US$16.0bn.

The leisure & entertainment (-28.7%, down US $6.6bn from 2019 to US$16.4bn), financial services (-18.2%, down US$8.7bn to US$39.2bn), retail (-15.2%, down US $10.2bn to US $57.2bn) and automotive (-11.4%, down US$7.4bn to US $57.6bn) sectors are all set to witness sharp declines this year.

WPP global president Brian Wieser said: “Opportunities can come from this crisis, both for advertisers and for media owners. Every brand should be questioning assumptions about their company’s competitive position. What are the ways in which you can reinvent the category? That the economy will be weak is a given, but any one business’s outcomes are not.”

“Online is not shielded from the downturn – internet growth will almost grind to a halt in 2020

TRENDS BY PLATFORM

- Alphabet: Alphabet’s advertising revenue – across Google Search, YouTube, and Google Network Members (third parties that host Google ads) – is forecast to rise by just 1.6% to $137.1bn this year – before the deduction of traffic acquisition costs (TAC), which amounted to $30.1bn in 2019. This means the company accounts for almost one in four dollars (24.4%) spent on advertising worldwide. The latest projection represents a downgrade of $12.9bn from WARC’s pre-outbreak forecast.

- Facebook: Advertisers are expected to spend $77.6bn across Facebook, Messenger, WhatsApp and Instagram this year, a rise of 11.5% from 2019. This marks a downgrade of $5.3bn from the pre-outbreak forecast and gives Facebook a 13.8% share of global advertising investment.

- Trends by media and format

- TV: Spend is forecast to fall 13.8% to $159.9bn, 28.4% of all global spend this year. A third of the global TV total is transacted in the US where, TV spend is set to fall 9.6% ($5.8bn) to $54.7bn despite a fillip from presidential campaign spending.

- Out of home: The OOH sector has suffered from a severe lack of reach during international lockdowns. Spend is expected to fall by 21.7%, or $8.7bn, in 2020 compared to a previous forecast of 5.9% growth.

- Cinema: Like OOH, cinema advertising has been heavily impacted by lockdown conditions. Brand investment is set to fall by almost a third (-31.6%) this year but should recoup these losses in 2021.

- Radio: Investment in radio ads is projected to fall by 16.2% – or $5.1bn – this year, compared to a pre-outbreak forecast of 1.8% growth.

- Newspapers: Spend on print newspapers is forecast to fall by $7.6bn, or 19.5% in 2020, compared to a pre-outbreak forecast of -5.9%.

- Magazines: Like newspapers, print magazines have been heavily impacted by reduced circulation. Advertiser spend will fall by over a fifth (-21.5%), or $3.4bn in 2020.

- Social media: Social formats, combined, are expected to be the strongest performers in 2020, recording total growth of 9.8% to $96bn. This does, however, represent a downgrade of $6.4bn when compared to WARC’s pre-outbreak forecast.

- Online video: Growth is forecast to ease to 5.0% (to $50.3bn) this year, equivalent to 8.9% of global advertising spend. YouTube is expected to account for three in ten cents.

- Search: Growth will ease to less than a percent (+0.9%) in 2020 after a downgrade of $14.1bn from February’s forecast.

- Trends by region

- North America: In North America, where 39.5% of global adspend is transacted, ad investment is expected to fall by 3.7% – or $8.5bn – to $222.5bn this year, encompassing a 3.5% fall in the US (down $7.7bn to $221.3bn) and a 6.5% dip in Canada (to $11.5bn). This compares to pre-outbreak forecasts of +8.8% and +1.9% respectively.

- Asia-Pacific: Advertising spend is expected to fall 7.7% ($14.4bn) to $173.5bn in 2020, 30.8% of the global total. China (-8.6%, down $7.5bn to $80.0bn), Japan (-6.4%, down $2.5bn to $36.2bn), and Australia (-8.2%, down $1.1bn to $11.9bn) are all set to record declines. Indian growth will ease to +0.7% to a total of $9.4bn in 2020.

- Europe: European adspend is forecast to fall by 12.2% ($18.1bn) to $129.9bn this year, with France leading key market decline at -18.7% (down $3.1bn to $13.4bn). The UK (-16.4%, down $5.1bn to $31.3bn), Germany (-6.1%, down $1.5bn to $24.9bn), Spain (-6.0%, down $500m to $6.6bn), Italy (-21.7%, down $2.1bn to $7.6bn) and Russia (-12.3%, down $1.2bn to $8.5bn) will also record sharp falls.

- Latin America: Adspend is set to fall 20.7% ($5.6bn) to $21.4bn this year, led by a sharp decline in Brazil (-22.5%, down $3.4bn to $11.5bn) where the COVID-19 outbreak has been particularly acute.

- Middle East: While not as severely impacted by COVID-19 as other regions, adspend in the Middle East is still set to fall 15.1% ($1.8bn) to $10.4bn in 2020, as oil-rich economies suffer from falling commodity prices.

- Africa: Spend is expected to fall 19.5% to $5.3bn this year, though this could be more severe if the outbreak worsens in the region.

A sample report of WARC’s Global Ad Trends: Covid019 & ad investment is available to download here. The full report is available to WARC Data subscribers.

Global Ad Trends, a monthly report which draws on WARC’s dataset of advertising and media intelligence to take a holistic view on current industry developments, is part of WARC Data, a dedicated independent and objective one-stop online service which rigorously harmonises, aggregates, verifies and evaluates data from over 100 reputable sources, including Nielsen, featuring current advertising benchmarks, forecasts, data points and trends in media investment and usage.

- More here: www.warc.com/data

Share this Post